Buy Now, Pay Later (BNPL) has transformed eCommerce over the past decade, fast becoming a go-to solution enabling businesses to improve customer experience, conversion and loyalty.

The concept is nothing new. Retailers selling ‘big-ticket’ items – such as furniture, household appliances, and cars – have allowed customers to pay in instalments for years. As a digital trend, however, BNPL has been pivotal in reshaping payments.

Today, there are more than 360 million BNPL users worldwide, with the global Buy Now, Pay Later market worth over $500 billion.

Buy Now, Pay Later and Banking-as-a-Service

Retailers looking to offer their own Buy Now, Pay Later solution have turned to Banking-as-a-Service (BaaS).

BNPL is effectively a loan typically repaid in instalments. So, the benefit of offering BNPL directly is that a brand keeps the customer in the ecosystem of their website or app, rather than seeing them taken to a third party to complete the transaction. The ability to integrate financial solutions like BNPL directly into the customer journey is the promise of embedded banking.

BaaS enables businesses to embed financial services when and where customers need them most. This gives the end customer greater flexibility and optionality when choosing their preferred payment method. Retailers and eCommerce marketplaces understand that for many consumers, greater choice at checkout is a non-negotiable – and they are increasingly turning away from vendors not offering BNPL.

Shopper behaviour and Buy Now, Pay Later

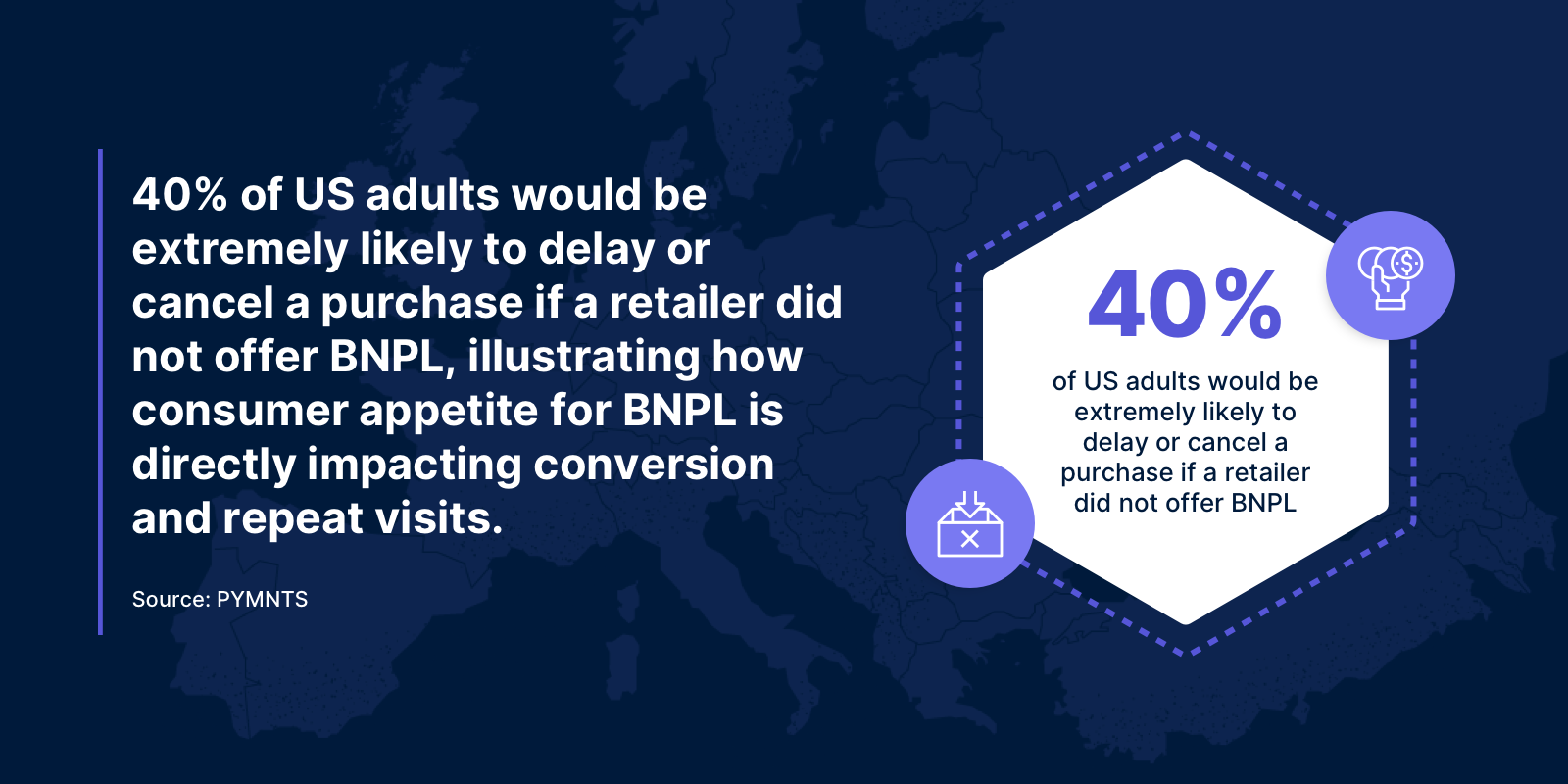

Data from recent years has illustrated how consumer appetite for BNPL is directly impacting conversion and repeat visits. A PYMNTS study of over 3,000 US adults cited two fifths of the respondents saying they would be extremely likely to delay or cancel a purchase if a retailer did not offer BNPL.

As well as abandoning their virtual shopping cart, it has been proven that consumers will ‘downgrade’ on items when BNPL is not available – opting for cheaper alternatives to the ones they originally intended to buy. A quarter (25%) of millennials and a fifth (19%) of Gen-Z said they make this choice.

The cost-of-living crisis has driven demand for BNPL upwards, as our own research last year showed. When Aion Bank/Vodeno commissioned a survey of more than 3,000 European consumers last year, we found that over a third (37%) were more likely to use BNPL and flexible payment options due to the cost-of-living crisis. BNPL allows customers to stagger and delay payments, alleviating cash flow challenges that have become particularly pronounced due to high inflation and rising interest rates since 2022.

More generally, our European study illustrated the relationship between BNPL and brand loyalty, with two in five surveyed claiming they would only stay loyal to brands that offer embedded banking products like BNPL.

Click here to learn about how BNPL is redefining the way consumers and businesses make purchases.

Exploring how Buy Now, Pay Later can help your business attract new customers

BNPL has the potential to allow businesses to attract new customers, both in the B2B and B2C space. Here’s why it appeals:

- Manage cashflow: the flexibility of splitting and delaying payments helps customers avoid large upfront costs and manage cashflow.

- Immediate access: people will typically save for major purchases (such as a new car or sofa) for months, if not years, whereas BNPL allows them to make that purchase immediately and then pay for it over time.

- Aspirational purchases: customers have the ability to opt for more aspirational brands.

- Retain cash: BNPL allows customers to retain their cash for longer, meaning they can save, spend or invest that money elsewhere before needing to make later repayments.

- Improve credit scores: if their BNPL plan reports on-time payments to the credit bureaus (like Experian) then that can boost their credit score.

In the B2B space, BaaS-powered merchant financing – essentially a B2B version of BNPL – is gaining traction amongst marketplaces in order to attract and keep the best vendors. Here, marketplaces can offer up-front capital to their merchants for the production or purchase of goods, with repayments drawn from the revenues of those goods once they are sold. With access to traditional forms of credit often difficult for small businesses, merchant financing offers the ability to easily access credit, combined with the flexibility of repayments aligned with their business model.

For more information on how BNPL can help your business attract new customers, click here.

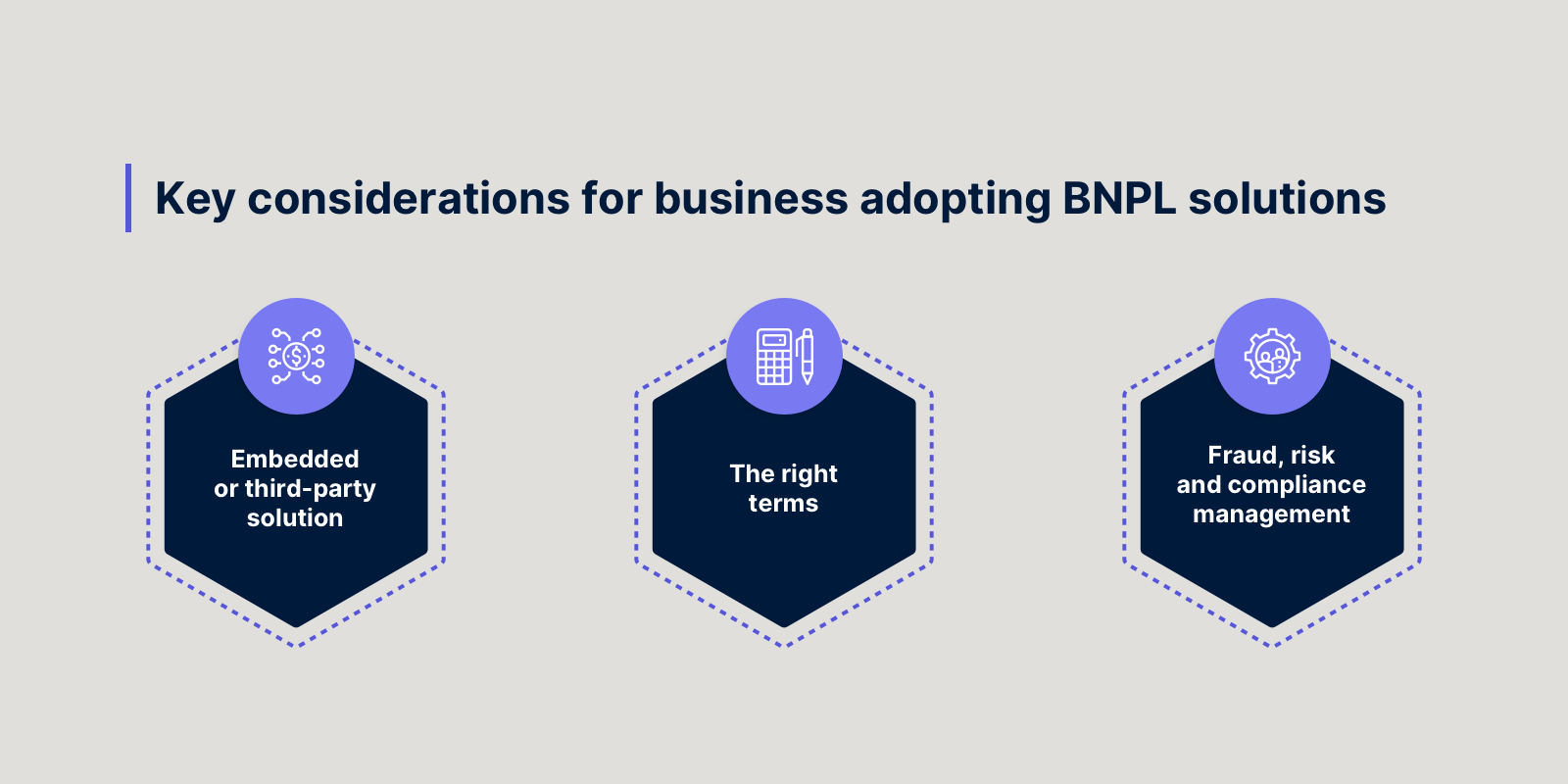

Key considerations for businesses adopting Buy Now, Pay Later solutions

BNPL is becoming table-stakes in eCommerce, but there are some key considerations before deciding who to partner with and how to deliver the solution to customers.

Both the solution and the BaaS provider must be the right fit for your business and your customers. Here are some of the key questions to answer:

- BaaS-powered embedded BNPL, or third-party solution?

Businesses have a choice between working with a BaaS provider to implement their own solution into the customer journey, or working with a third-party provider to use an off-the-shelf solution at checkout. Doing the latter will require a customer to submit their personal details to that third party, affecting the customer experience and lessening the control that the business maintains over the BNPL product and how it works.

- What are the right terms?

Adopters need to ensure the terms of their BNPL products – how many instalments over how long, and what interest is charged – fit with their customers’ needs and the products they are selling.

- How to manage fraud, risk and compliance?

BNPL is a form of credit, and those offering it must ensure risk is managed carefully so that neither they nor their customer is irresponsibly exposed. Adopters must ensure that their chosen partner provider actively mitigates risks through robust credit assessments, advanced fraud detection mechanisms, and proactive monitoring.

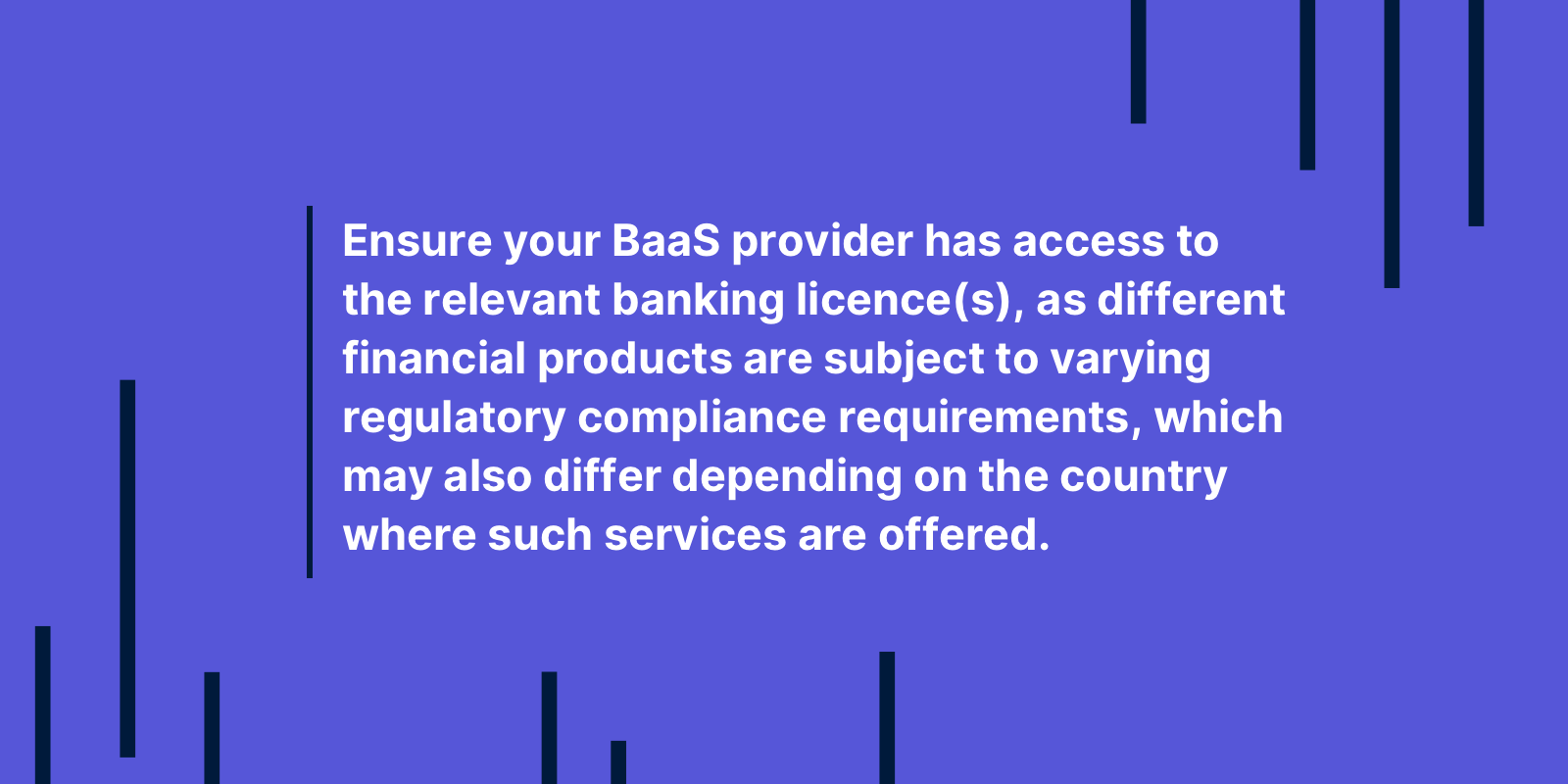

Any businesses considering BaaS must be aware of the importance of the regulation and compliance aspects of financial services, and they should not assume that every provider will take care of this for them. In reality, which banking licence (if any) a BaaS provider has dictates the services they are able to offer just as much as their underlying technology. What’s more, when picking the right BaaS partner, businesses should closely scrutinise their compliance and risk management credentials; this will have a marked impact on the outcome.

Different financial products are subject to different regulatory compliance requirements, which may also vary depending on the country where such services are offered. This means that, when choosing a BaaS partner, companies should – first and foremost – ensure their BaaS providers have access to the relevant banking licence. While basic payment solutions are often simple to offer, lending products like BNPL are more intricate due to evolving regulations and the complex credit evaluation process for offering loans to consumers.

Again, depending on which solutions a business intends to integrate – payments or credit, insurance or savings – this would dictate the banking licence their BaaS provider should hold.

Read our useful guide on how to pick the right BNPL partner for your business.

Get in touch with Vodeno

BNPL can help businesses attract and retain customers, help with conversion, increase basket size and order frequency, and enhance loyalty. However, effectively implementing the right solution requires the right provider.

Aion/Vodeno offer end-to-end BaaS – a full tech stack and banking licence – with Aion’s ECB licence enabling a comprehensive suite of banking products, underpinned by the Vodeno Cloud Platform. We also understand customer journeys. We embed financial services that give clients the ability to improve their experience, meet their customer needs, and drive loyalty.

Get in touch with Vodeno today to learn about our BaaS-powered embedded finance solutions, including BNPL, and how they could transform your business.