Banking-as-a-Service (BaaS) has been the subject of a huge amount of hype over recent years.

It is a chicken-and-egg scenario – hard to say whether the hype is the cause or result of ever-larger predictions from market analysts for the Banking-as-a-Service industry’s total addressable market (TAM) size, but there is no shortage of bold forecasts. McKinsey, for example, expects the European BaaS TAM to reach a value between €90 billion and €105 billion by the year 2030.

Strong consumer appetite for embedded banking products is largely driving these predictions, with two factors that are closely intertwined:

- eCommerce companies have sought a competitive edge after the pandemic boom, turning to Banking-as-a-Service – powered embedded banking to improve customer journeys, boost loyalty and increase revenue. Embedded payments and buy now, pay later (BNPL) have been the most common use cases.

- Meanwhile, consumers, particularly Millennials and Gen Z, have become increasingly comfortable accessing banking products directly from the brands they already use and trust. In fact, our recent research found that (52%) of 25-34-year-olds prefer using financial products and services from their favourite brands over traditional banks, while 50% will only stay loyal to brands offering embedded financial products and flexible solutions like BNPL and cashback.

The result is that Banking-as-a-Service has evolved from a nascent concept to being a truly disruptive market force helping to innovate customer journeys across multiple sectors. Today, businesses are using BaaS to attract new customers, increase basket size, improve retention and loyalty, and generate new revenue streams. And customers are benefiting from frictionless experiences, underpinned by greater choice and access to banking products at the point of need.

Crucially though, Banking-as-a-Service continues to evolve at pace, and in 2024, there has been a marked step forward. First-generation BaaS, or BaaS 1.0, has been defined by a rush to capitalise on the trends noted above. Now, this ‘fintech-led, investor-fuelled, growth at all costs’ without much thought to regulation version of BaaS is dead, or is dying a very quick death as regulatory scrutiny intensifies.

We are entering the more responsible, sustainable age of Banking-as-a-Service 2.0 – a positive development for the BaaS industry.

Regulatory compliance comes under the microscope

To date, regulatory compliance has too often been overlooked in Banking-as-a-Service, with insufficient focus given to the fact that not all BaaS providers are the same: some are strictly IT specialists, others hold EMI or payment licences, while just a select few – Aion/Vodeno is one – can offer services based on a full banking licence.

A Banking-as-a-Service provider’s banking licence (if they have one at all) dictates the services they are able to offer just as much as their underlying technology. What’s more, the compliance and risk management credentials of BaaS providers are not consistent. Businesses considering BaaS must be aware of the importance of the regulation and compliance aspects of financial services, and they should not assume that every provider can or will take care of this for them.

This can be confusing for companies considering BaaS, and regulators are now much more closely at the sector. In practice, regulatory compliance in BaaS should be table stakes, with banks – the underlying licence holder – owning the customer relationship from a regulatory perspective. But, that’s not always been the case.

Greater focus on regulatory compliance is the defining premise of Banking-as-a-Service 2.0…let’s drill further down into this next era of BaaS.

What will BaaS 2.0 look like?

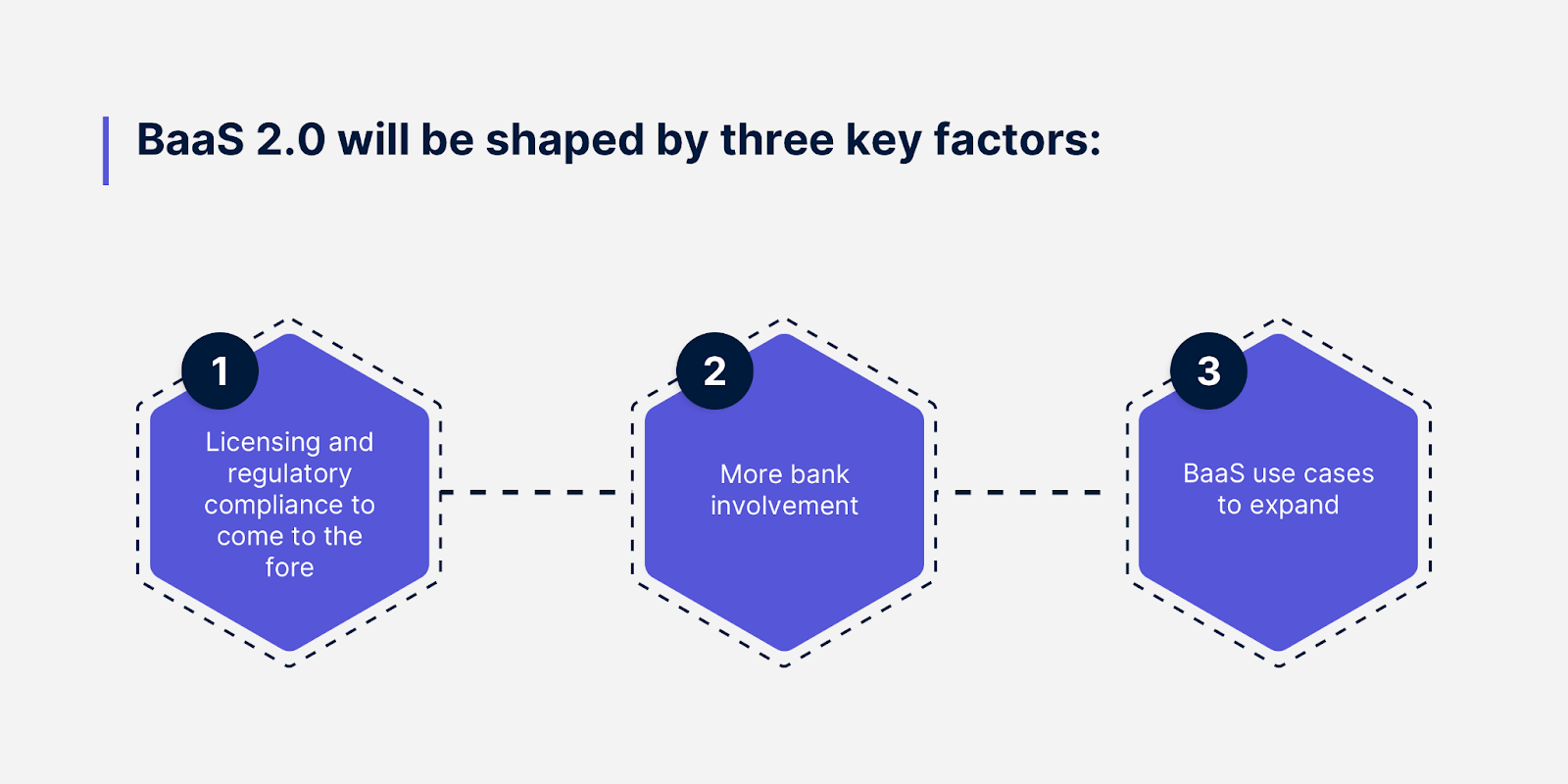

BaaS 2.0 will be shaped by three key factors:

- Licensing and regulatory compliance to come to the fore

As noted, as we enter the next chapter of the Banking-as-a-Service story, businesses seeking a BaaS partner will focus on how the BaaS provider is licensed, alongside their technology solution.

Additionally, as BaaS matures, businesses considering opportunities in this space must be aware of the importance of the regulation and compliance aspects of financial services.

Compliance processes such as Know Your Customer (KYC) and Anti-Money Laundering (AML) are integral in the delivery of banking products. Adopters will seek out Banking-as-a-Service providers with demonstrable experience and expertise to handle this across multiple markets and jurisdictions. Here, we may see artificial intelligence play a far greater role in automating processes, while also ensuring a smoother customer journey for the end user.

- More bank involvement

Banking-as-a-Service 2.0 will also see more investment from larger banks. The appetite for BaaS and embedded banking is clearly there – both from businesses adopting the solutions and end customers using the products. And, big banks are starting to believe in the BaaS model as a cost-effective path to acquire customers at scale via a B2B2C model.

Banking-as-a-Service will be central to the future of banking – not with banks and BaaS providers existing as separate entities, but rather with BaaS sitting parallel to traditional banking. UniCredit’s recent agreement to acquire Aion Bank and Vodeno exemplifies this – it is the first instance of a major European bank recognising the BaaS model as a future growth opportunity, and, therefore, investing in its development.

More investment in BaaS will mean more innovation and more adoption across different sectors. We will likely see more interest from larger banks in the years to come.

- BaaS use cases to expand

Embedded payments and lending are the foremost BaaS use cases. This makes sense: the ability to offer a quick and frictionless experience when processing transactions is the foundation of any good customer experience.

Over the coming months and years, a wider variety of use cases will emerge, including digital wallets, savings and investments – all integrated directly into the customer journeys of the biggest brands. The goal: To create more value for the customer and retain loyalty.

Much has been said about BaaS impacting conversion, but the real NorthStar of BaaS is to influence the browsing stage, with tailored financial products determined via data analytics, offered in a contextual way throughout the shopping journey. This will help foster a better, more loyal – and long-term – customer relationship.

Do you want to learn more about the future of Banking-as-a-Service, or to discover how embedded finance could transform your business or industry? Then get in touch with Vodeno today.