Research predicts that the embedded lending market will exceed USD 32.5 billion by 2032. But, what is embedded lending? And, how do Banking-as-a-Service (BaaS) providers offer it?

While most consumers are already familiar with Buy Now, Pay Later (BNPL) and split payment options integrated within the checkout journey of their favourite brands, many BaaS providers are expanding their portfolio of lending products, with both B2B and B2C use cases.

Here, we explain the different types of BaaS lending products on offer, and how these solutions work.

Types of BaaS lending products

Buy Now, Pay Later

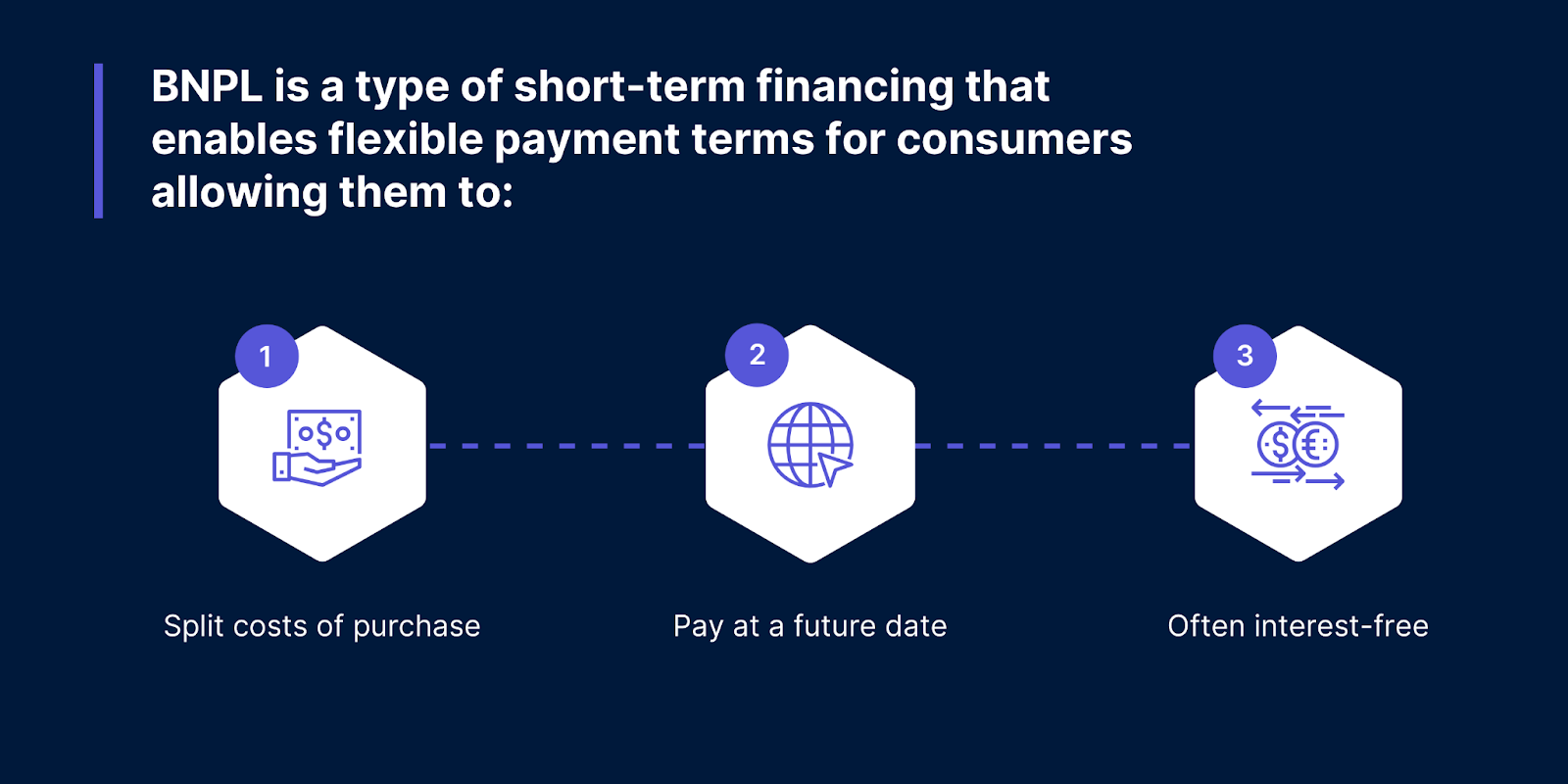

BNPL is a type of short-term financing that enables flexible payment terms for consumers, allowing them to split the cost of their purchases and pay for them at a future date, often interest-free. It is a great example of embedded finance in play, and the coming together of the retail (“buy”), payment (“pay”) and financial services and credit (“later”) industries.

At its core, BNPL relies on instant credit and risk management decision engines that operate in real-time in the live marketplace and that ultimately improve the shopping and purchasing experience of both customers and merchants while being sticky enough to have them return to the service regularly. According to Juniper Research, 360 million consumers across the globe used BNPL in 2022, and this number is expected to grow to more than 900 million by 2027. In turn, retailers can expect a 20-30% increase in conversion.

Decoupled debit card

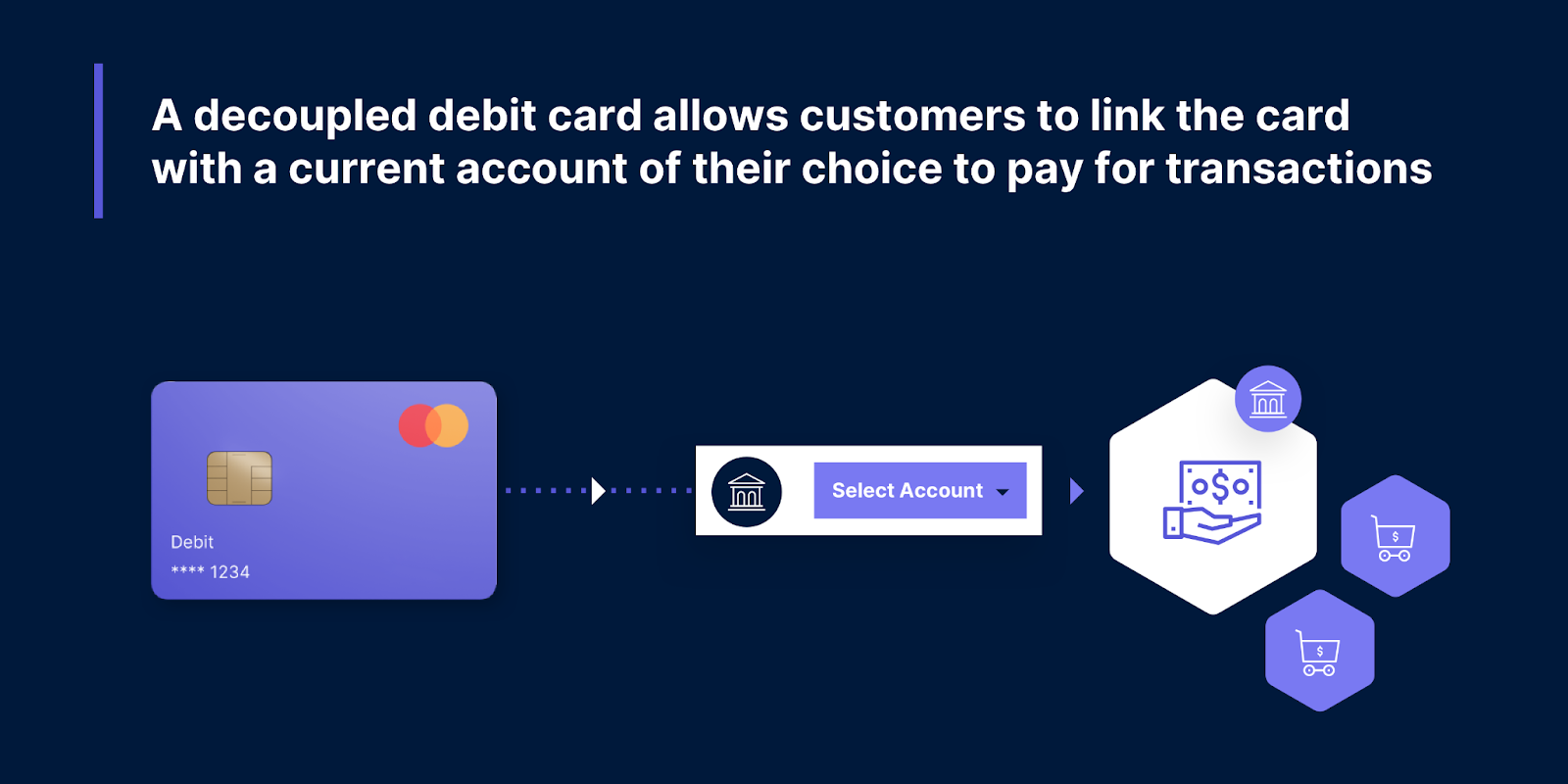

A decoupled debit card allows customers to link the card with a current account of their choice to pay for transactions. Decoupled debit eases the friction of adopting a new card because the user does not need to open a new account or top-up funds in order to use the card. Additionally, brands can layer on additional benefits like cash back and loyalty to incentivise card usage.

Our work with METRO Financial Services, a subsidiary of leading German wholesale firm METRO AG, shows that decoupled debit can solve customer pain points and boost customer loyalty.

METRO’s decoupled debit card aimed to solve their customers’ specific business challenge – cash flow issues. The card offered flexible lending options and up to 1% cashback, and it could be used anywhere METRO customers shopped. The decoupled nature of the product made it easy to use, and the flexible lending products empowered customers to choose payment options in line with their business cash flow.

Merchant Financing

Merchant financing is a lending solution that marketplaces can offer their vendors. It offers up-front capital that merchants can use to produce or buy goods, with repayments drawn from the revenues of those goods once they are sold. Essentially a BNPL product for SMEs, merchant financing offers the ability to easily access credit, combined with the flexibility of repayments aligned with revenues.

This is invaluable to small business owners that make up marketplaces, as the process of obtaining credit from traditional banks can be cumbersome; additionally credit from merchant financing is based on turnover history.

For marketplaces, offering this service allows their vendors to grow their business, creating long-term brand affinity and stickiness. With marketplace spending predicted to exceed $2 trillion by 2023, platforms have a vested interest to offer value-added services to support their vendors and keep their best ones loyal to them. Offering innovative financial services can meet this need, while creating additional revenue streams and attracting new vendors.

Debt receivable financing

Businesses that offer lending products may find themselves capital constrained, limiting their ability to grow. To these businesses, debt receivable financing offers a route to scale and growth. Vodeno/Aion works with lending businesses to purchase the unpaid invoices (debts) of their existing loan book (receivables), which frees up their capital to acquire more customers.

Vodeno/Aion are able to offer this service because Aion is a fully licensed bank – regulated by the National Bank of Belgium – with a strong balance sheet. What’s more, debt receivable financing can be more cost-effective for businesses in search of capital than expensive traditional bank loans or additional investment funding.

Our partnership with Danish fintech MoneyFlow demonstrates the value of debt receivable financing as a route to business expansion. Founded in 2018, MoneyFlow enables SMEs to sell their invoices and access their future revenue, helping many to navigate the delays and outstanding payments that put a strain on their business. Through our partnership, MoneyFlow are expanding their services in the Nordics and throughout Europe.

How BaaS lending works at Vodeno/Aion

Currently, we are one of the only BaaS providers on the market equipped to offer a full scope of BaaS products, including lending products, in a flexible, modular solution. Unlike other providers on the market, we give our clients access to services based on a full ECB banking licence, alongside the compliance and security of a European bank, provided by Aion Bank. This means that we are uniquely positioned to offer a comprehensive suite of BaaS solutions to both regulated and non-regulated entities, with the way we offer Lending-as-a-Service being a key differentiator – Aion’s banking licence and balance sheet means we are able to offer multiple lending products in a fully end-to-end digital way with the flexibility to offer capital and credit risk assessment based on the client’s preferences.

Arrange a call today to see how we can support your embedded finance journey.